Aaron Foyer

Director, Research

How has North America circumvented the global gas crisis?

Aaron Foyer

Director, Research

Regulars of the Japanese bathhouses known as sentōs are not having a good war.

The origin of the sentō dates back the 700s, when Buddhist monks dipped in public baths, not just to cleanse the body but also to purify the spirit. They essentially became the church hall of feudal Japan, where the sacred and the communal merged.

“Skinship” is the Japanese idea that physical closeness builds emotional closeness, making public baths a key part of the country’s social fabric. The term “hadaka no tsukiai” or “naked friendship” refers to kind of honest, status-free relationship that can only form when everyone is without their clothes. A CEO and a janitor in a sentō are just two naked people in hot water.

Source: Metropolis Japan

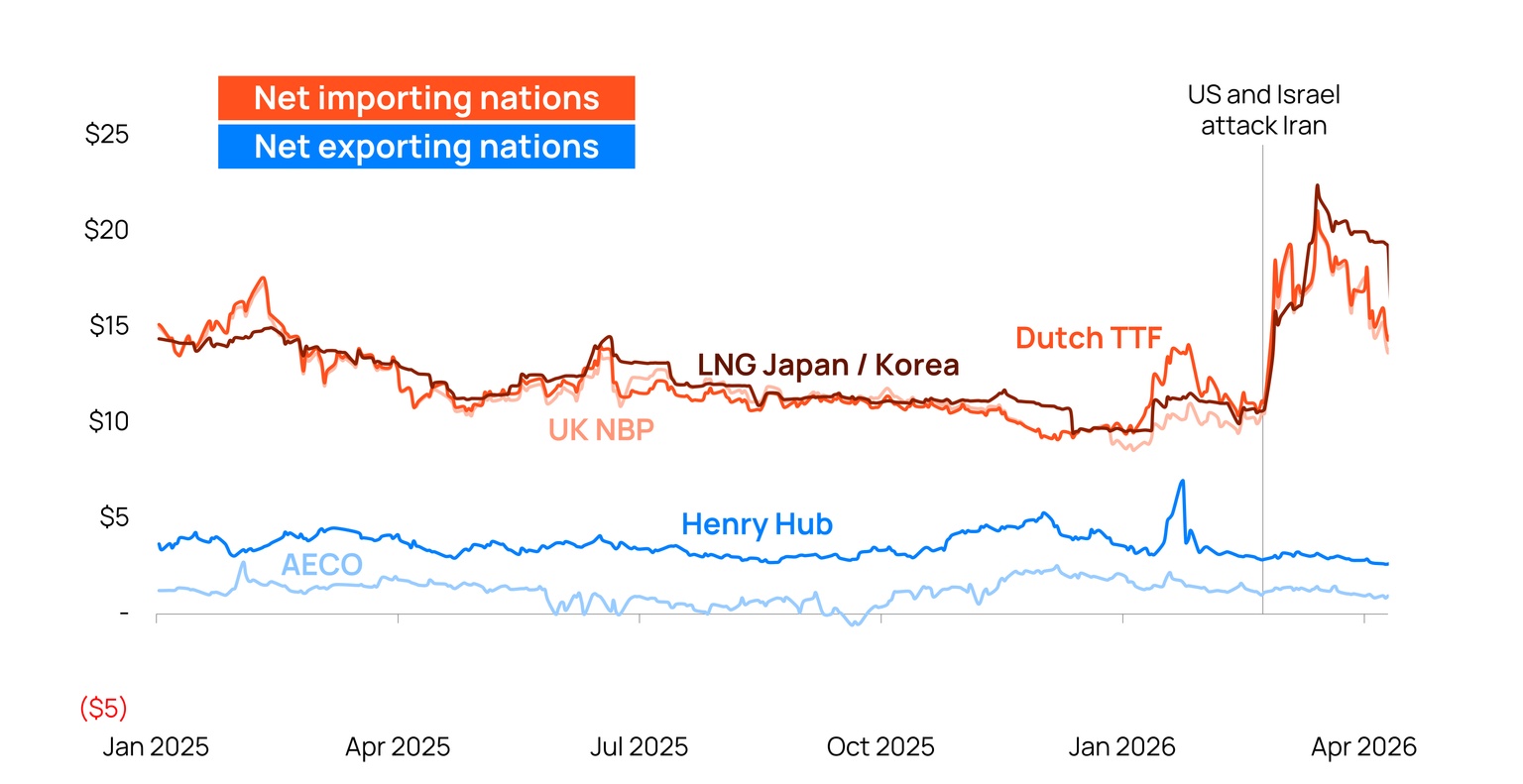

But Japanese bathhouses have had a rough go of it since the start of Iran war in late February, with 30% of sentōs today relying on traditional oil or gas boilers to heat their bath water. Prices for LNG sold to Japan are up 55% since the start of the war, having more than doubled in the early days of the conflict.

As a result, many sentōs have been forced to shorten their operating hours or charge more to stay afloat, while others have been forced to close their doors entirely. The popular Katsuragi Onsen sentō in the northeast city of Aomori will close its doors in May because of rising energy costs.

Broader impact: It’s not just those trying to cleanse their spirits who have been impacted by the energy crisis: Prices have spiked around the world. At their height, both the Dutch TTF and UK NBP gas prices in Europe had jumped 50% from pre-war levels and remain high.

Source: Oilprice.com

But it’s a completely different story in North America. The price for Henry Hub, the key North American gas marker, has barely budged since the start of the war. The EIA actually lowered its forecast Henry Hub 2026 price in its April Short-Term Energy Outlook. But why?

How has North America been able to grow the most impressive gas production on the planet, lead global LNG supplies and circumvent the global gas crisis? Let’s fire up the sentō boilers and find out.

Natural gas in North America is a fortress, though a surprising one.

On paper, neither the US nor Canada looks like a gas superpower. The US ranks fifth globally in proven reserves, just a third of Russia's. Canada ranks ninth, with just a fifth of America’s.

But what sets the continent apart is ingenuity. The combination of horizontal drilling and hydraulic fracturing that was mastered by the industry in the early 2000s paved the way for one of the world’s great energy revolutions.

Vive La Revaporization: In 2000, US gas production was in decline and the country was building regasification terminals to handle the LNG imports it assumed were coming. Twenty-five years later, those same terminals have been converted to export facilities and the US and Canada now produce nearly 30% of the world's gas, far more than they use.

Sources: US Energy Information Administration, Canadian Energy Regulator

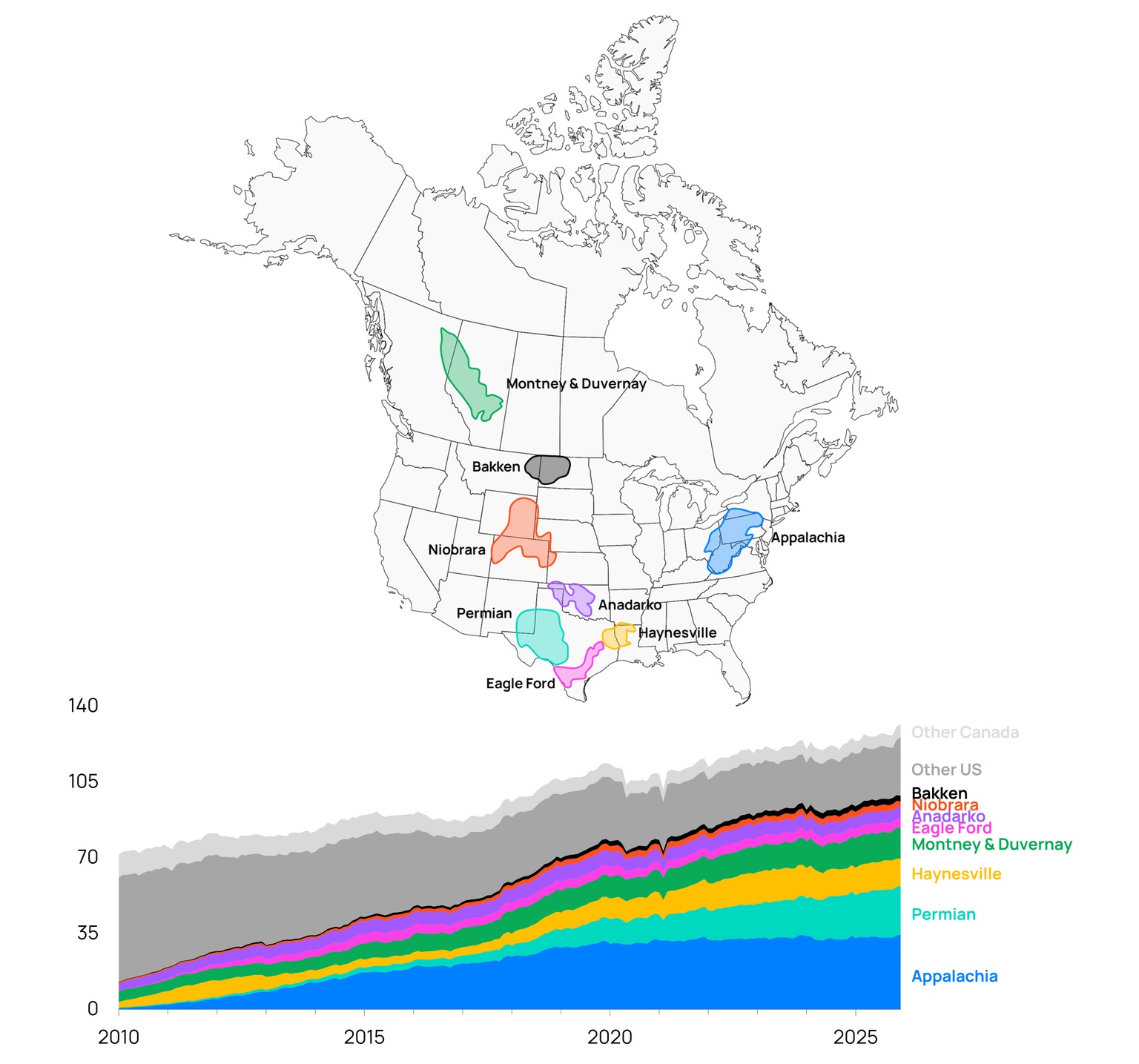

And unlike many of the other global gas leaders, where a single gas field often accounts for most of the country’s production, Fortress North America has many pillars to rest on:

With pipelines that connect the various plays from Dawson Creek to Dallas, natural gas in North America works like its own giant market.

Source: US Energy Information Administration, Alberta Energy Regulator

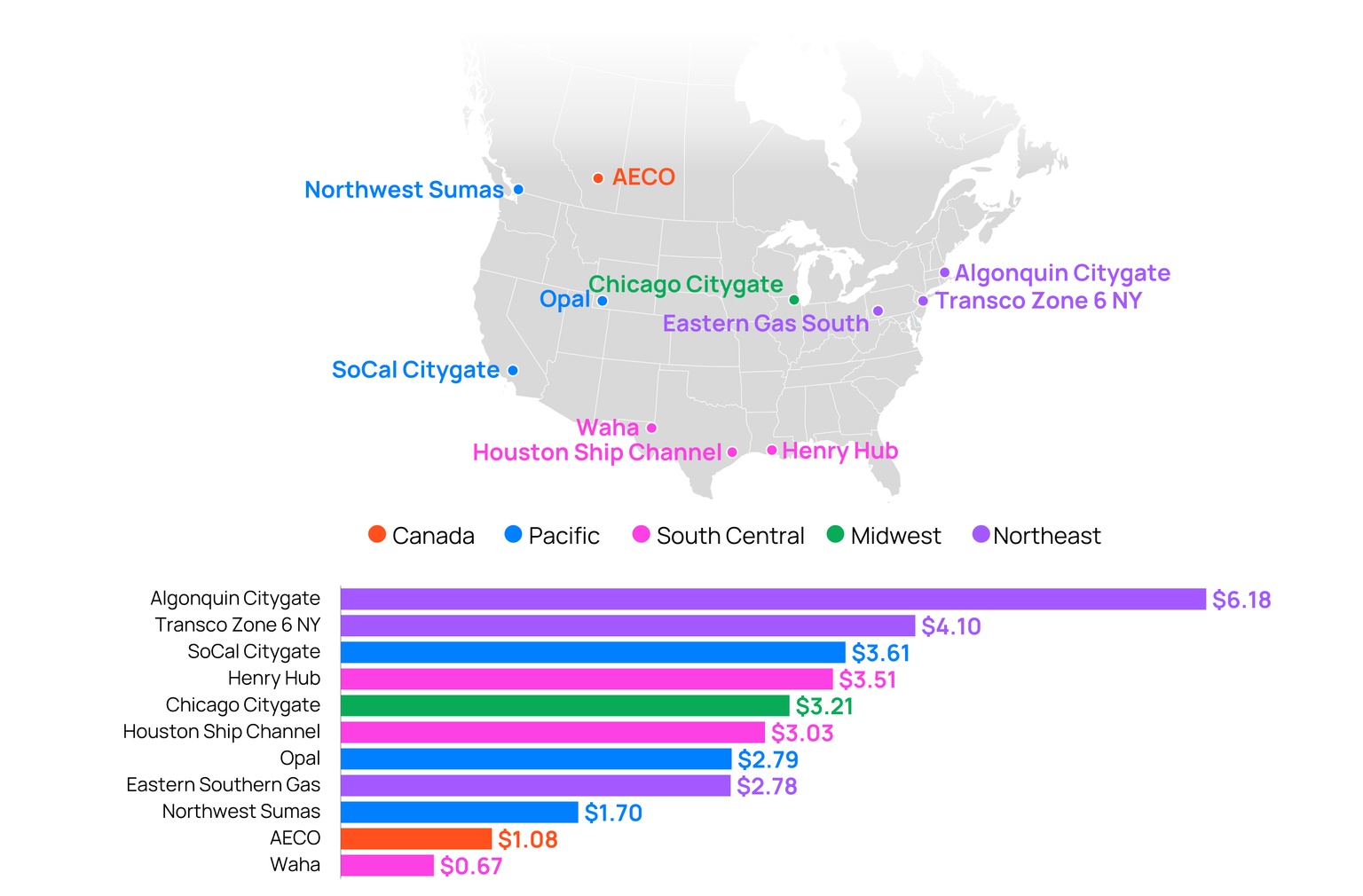

The fact that natural gas is a regional commodity has helped insulate North America from the gas and power price spikes seen around the world.

When a region outproduces its needs, there’s only so much that can be done with the gas. With storage levels already well above their five-year average in both the US and Canada, that leaves sending it abroad.

Gas, chilled: The modern liquefied natural gas export era owes its due to Charif Souki, the Egyptian-born American businessman and former banker who foresaw America’s export potential before nearly everyone.

Founding Cheniere Energy in Houston in 1996, Souki made a bet-the-company move and flipped its business model to export gas. Cheniere converted its Sabine Pass terminal from an import facility into what became the first large-scale LNG export terminal in the contiguous United States. In February 2016, the first commercial shipment of LNG sailed from Sabine Pass en route to Brazil. It only took a decade from then for the US to become the largest LNG exporter in the world.

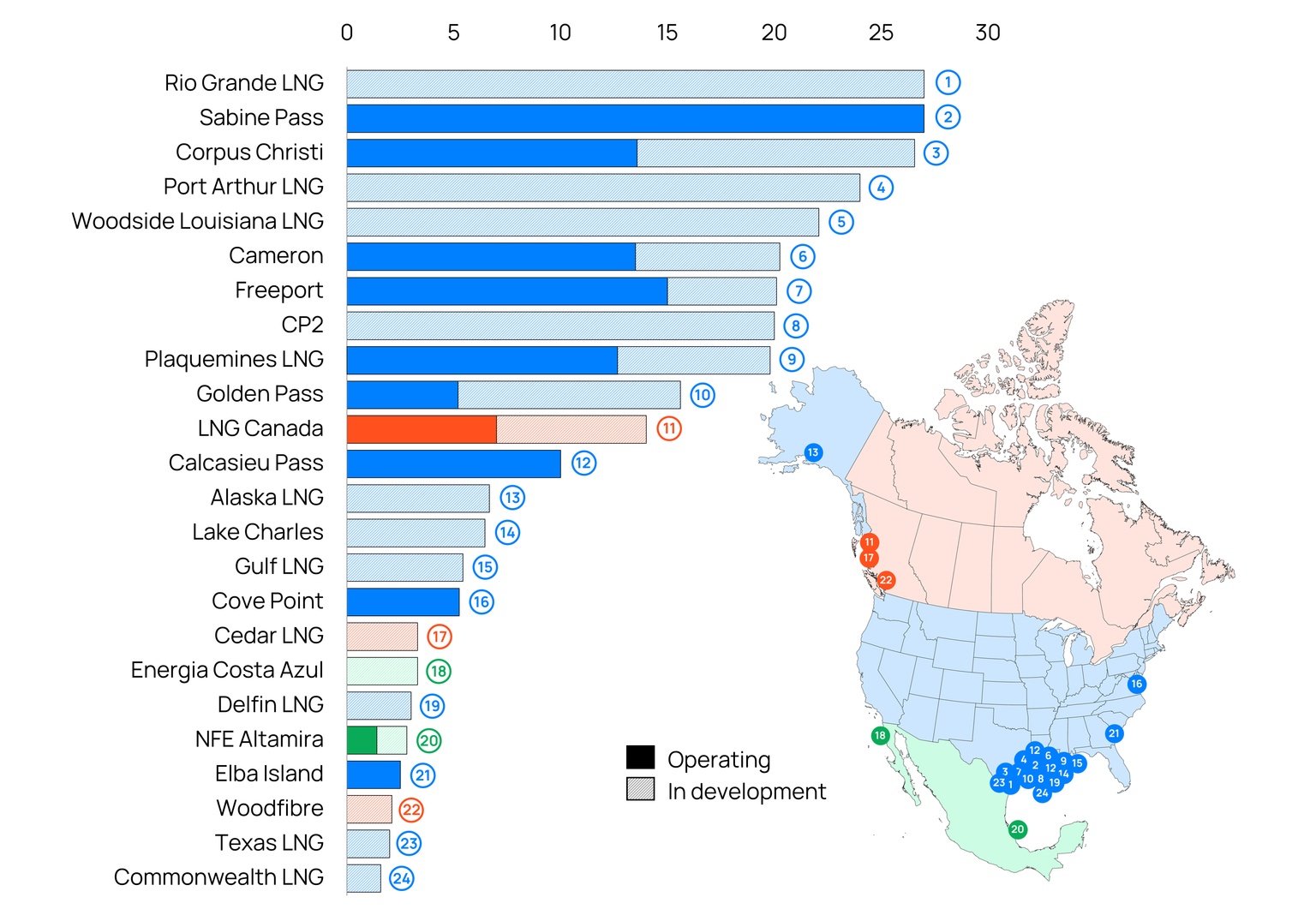

With the Golden Pass LNG facility coming online last month, there are now seven active export facilities in the US plus one in both Canada and Mexico. And it continues to grow, with several facilities expanding and others being built.

Source: US Energy Information Administration, public disclosures

Unfortunately, there’s little the US can do to respond to what’s happening now in the Middle East, with all the available LNG facilities running harder than Golden Tempo in Kentucky. The US Energy Information Administration expects up to 2 billion cubic feet per day of new American LNG production this year, but that’s well short of the 10 billion lost from Qatar.

The gatekeeper of power: The price of gas is also arguably the most important factor impacting electricity prices across much of the US and some parts of Canada.

In many power markets, the last unit of power needed to meet demand sets the price. Because gas plants sit at the intersection of “flexible enough to ramp” and “expensive enough to matter,” they are responsible for setting the price of power more than any other source.

As gas prices have stayed flat, electricity prices have not spiked, in contrast to the major economies of Europe and Asia.

Two flies in the low-price gas ointment are data centers and future LNG.

By the end of the decade, somewhere in the neighborhood of 50 gigawatts of new gas plants could come online in North America to help meet data center needs. Add to that nearly 64 million tons per annum of new LNG facilities that could be online by then, and it’s not hard to see a world five years from now with 15 billion cubic feet per day of additional gas consumption, roughly an eighth of what US and Canadian produce today.

Bottom line: While we might feel some collateral damage of the war in Iran at the pump, our utility bills have largely been spared.

It might not be skinship, but there is a closeness between the US and Canada in the two country’s gas markets. Mastering tight gas production two decades ago ended up being a shield from the otherwise global natural gas crisis.

The sentō boilers in Aomori may be going cold. North America's are running just fine.

+Bonus infographic: The Top Natural Gas Producers in North America

Insights for an evolving energy landscape delivered to your inbox.